Visa vs Mastercard vs RuPay vs Amex: What Is a Card Network? | CredClub Digital

Visa vs Mastercard vs RuPay vs Amex - What Is a Card Network and How Do They Actually Work?

Every time you tap your card, four invisible parties settle the transaction in milliseconds. One of them, the card network owns the rails, sets the rules, and earns a fee on every single swipe. Here is the complete breakdown, from a BFSI and Fintech lens.

What Is a Card Network? (The Foundation)

Card networks - also called payment networks or card schemes are the infrastructure layer that sits between your bank (the issuer) and the merchant's bank (the acquirer). They own and operate the messaging rails that make card transactions possible.

Every time you swipe, tap, or enter your card details online, here is what actually happens in under two seconds:

- Your bank (issuer) receives an authorisation request via the card network

- The card network routes that request to the merchant's bank (acquirer)

- Approval or decline flows back through the same network

- Settlement happens at end of day, again through the network

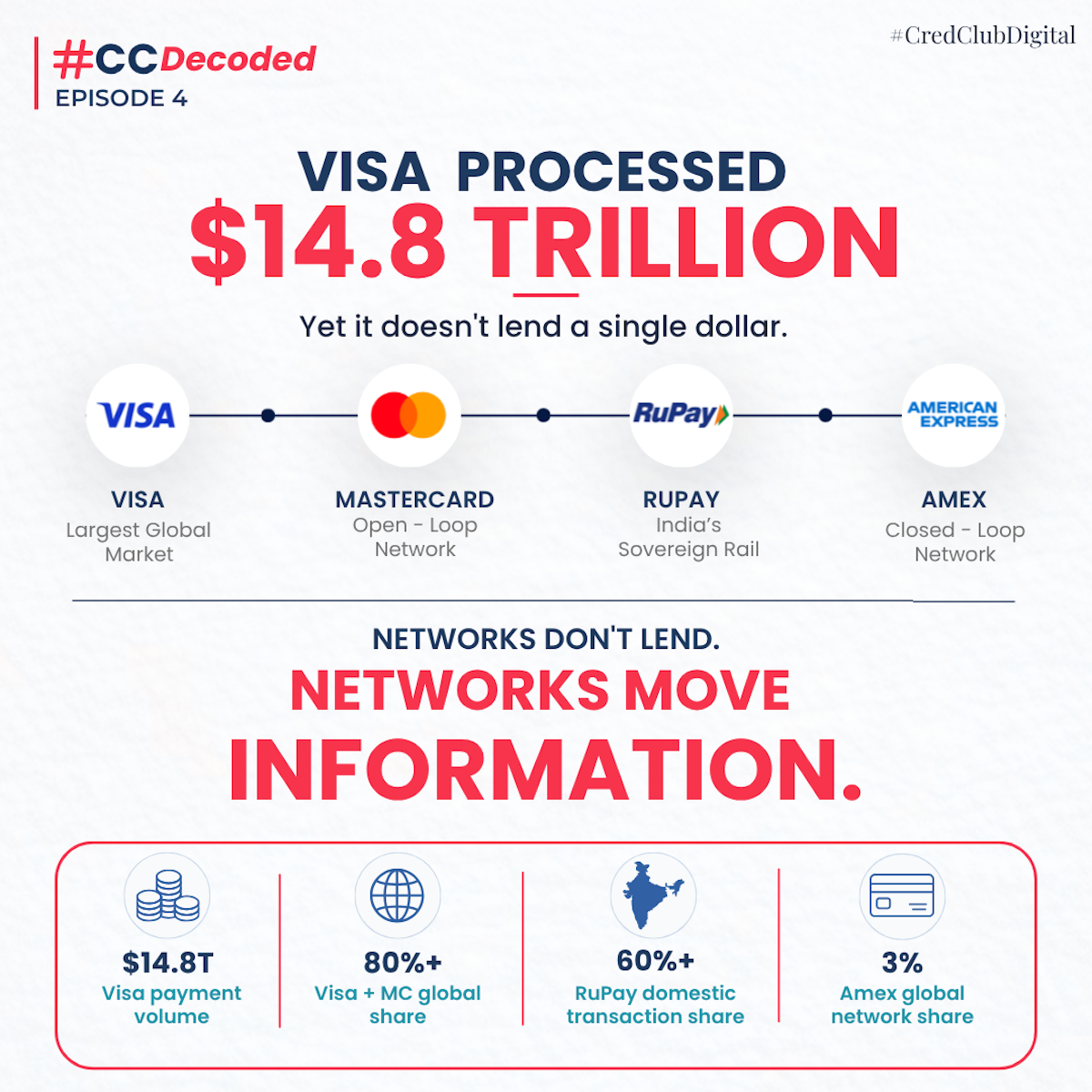

Card networks do not lend you money. They do not hold your deposits. They are pure infrastructure and they earn a small assessment fee on every transaction, multiplied by billions of transactions globally.

Visa: The World's Largest Card Network

Visa is the largest card network by purchase volume globally, with approximately 4.31 billion payment cards in circulation.

Visa operates on an open-loop model meaning it does not issue cards directly. Any bank, credit union, or NBFC can partner with Visa and issue a Visa-branded card to its customers. Visa's job is purely to own the rails, set the rules, and process the transaction.

Key facts about Visa:

- Historically dominant in India and the United States

- Earns a small assessment fee (typically 0.09%–0.13%) on every transaction, tiny per swipe, enormous at scale

- Sets interchange rates and dispute resolution processes that all issuing banks must follow

- Competes with Mastercard on acceptance breadth, technology investment, and issuer incentives.

- Offers tiered card variants - Classic, Gold, Platinum, Signature, Infinite each with different interchange rates and cardholder benefits.

For a cardholder, the Visa logo primarily signals global acceptance. For a bank choosing a network partner, Visa's economics, fraud infrastructure, and technology capabilities matter far more than the logo.

Mastercard: Visa's Closest Rival

Mastercard is the world's second-largest card network and, like Visa, operates a pure open-loop model. Mastercard has the broadest international reach by country count and growing share in tokenization and digital identity.

The Visa vs Mastercard debate is one of the most frequently asked questions in personal finance and the honest answer is: for most cardholders, the difference is minimal.

Both networks offer:

- Global acceptance at hundreds of millions of merchant locations

- EMV chip, contactless, and tokenisation security

- Chargeback and dispute resolution frameworks

- Tiered card variants with co-brand and rewards programmes

Where they differ meaningfully is behind the scenes in the economics offered to issuing banks. Mastercard has historically been stronger in Europe; Visa in India and the United States.

In recent years, Mastercard has steadily increased its market share globally, growing from around 22% to 27.41% of global card purchase volume.

For BFSI professionals choosing a network partner for a new card programme, the real differentiators are: interchange economics, co-brand incentives, fraud tooling, and tokenisation capabilities. The network logo is the last consideration.

American Express: The Closed-Loop Exception

Amex operates on an entirely different philosophy from Visa and Mastercard. American Express is a closed-loop network that issues most of its own cards, charges higher merchant fees, and concentrates on premium and corporate segments.

In a closed-loop model, Amex is simultaneously the network, the issuer, and sometimes the acquirer. It controls the entire transaction chain which means it captures more economics per transaction than Visa or Mastercard ever could.

How this plays out in practice:

- Amex sets higher interchange rates than Visa or Mastercard - typically 2.5%–3.5% for merchants.

- Higher merchant fees fund richer cardholder rewards, lounge access, concierge, travel perks.

- Lower merchant acceptance results from those higher fees — not all merchants want to absorb 3%+

- Amex cardholders are, on average, higher spenders, making the lower acceptance rate commercially tolerable.

Amex's closed-loop model means disputes are handled internally rather than through the merchant-acquirer-network-issuer chain that governs Visa and Mastercard chargebacks, giving Amex more unilateral authority in dispute outcomes.

In India, Amex has a smaller footprint than Visa or Mastercard but maintains a loyal, high-spending cardholder base. Amex has doubled down on lifestyle value less about where you can swipe, more about what you unlock.

The CredClub Digital insight: Amex's model proves that the most profitable card business is not the one with the most transactions it is the one with the highest-value transactions and the tightest control over the economics at every step.

RuPay: India's Sovereign Card Network

RuPay is the most strategically important card network you may know least about and that is changing fast.

RuPay (a portmanteau of Rupee and Payment) is an Indian multinational financial services and payment system, conceived and owned by the National Payments Corporation of India (NPCI). It was launched in 2012 to fulfil the Reserve Bank of India's vision of establishing a domestic, open, and multilateral system of payments.

The genesis of RuPay was explicitly geopolitical. It arose from the absence of a domestic price setter, which caused Indian banks to bear high costs for affiliation with international payment systems like Visa and Mastercard. India needed its own network one where payments data stayed within Indian borders, processed on Indian infrastructure.

RuPay by the numbers in 2026:

- RuPay now makes up one-third of all credit cards in India and handles about 25% of total transactions in the country.

- RuPay's credit-card market share rose from 3–4% pre-UPI linkage to approximately 16–18% by late 2025, driven largely by UPI usage.

- RuPay handles ₹18,000 crore in UPI transactions and ₹35,000 crore in total spending each month.

- By October 2024, approximately 750 million transactions worth ₹63,825 crore had been processed via RuPay credit cards on UPI since the feature launched.

The game-changer: RuPay Credit on UPI

In 2022, the RBI permitted RuPay credit cards to be linked to UPI giving credit card functionality to the 350 million+ Indians who transact daily on UPI QR codes, but had never used a card POS terminal. More than 5 crore merchants accept UPI QR codes, and many small merchants don't use POS machines — linking credit to UPI made credit usable where cards weren't before.

The interchange structure that makes this work:

RuPay credit cards carry approximately 2% interchange above ₹2,000 — split roughly 1.5% to the issuing bank and 0.5% to the network — while transactions at or below ₹2,000 carry zero interchange.

Why RuPay is geopolitically critical:

RuPay processes transactions fully within India this reduces latency and regulatory risk, lowers compliance friction for banks, and improves transaction success rates for users. India's payments data stays within India's borders. For a country of 1.4 billion people, that is not just a technical detail. It is a matter of financial sovereignty.

Mastercard and Visa have raised concerns with the Office of the United States Trade Representative (USTR) over India promoting the use of RuPay which tells you everything about how seriously the global networks are taking RuPay's rise.

The Business Model: Why Card Networks Are Among the Most Elegant in Finance?

Card networks earn money in three primary ways:

1. Assessment fees: a tiny percentage (0.09%–0.14%) charged on every transaction processed on their network. Tiny per transaction. Multiplied by trillions of dollars in annual volume, it becomes a cash machine.

2. Cross-border fees: a higher fee (typically 0.8%–1.0%) on international transactions, where the issuing bank and acquiring bank are in different countries.

3. Data and technology services: fraud analytics, tokenisation, identity verification, and consulting services sold to banks, governments, and merchants.

The genius of the model:

- Card networks carry no credit risk as they don't lend the money

- They hold no deposits - no balance sheet risk

- They own no branches - purely digital infrastructure

- They earn on every transaction regardless of whether the cardholder pays their bill or defaults.

Which Card Network Is Best for You in India in 2026?

Choose Visa or Mastercard if:

- You travel internationally frequently

- You want the widest merchant acceptance globally

- You want access to premium co-branded rewards cards from HDFC, SBI, ICICI, or Axis

Choose RuPay if:

- Most of your spending is domestic

- You want to use your credit card via UPI QR codes at small merchants

- You want lower annual fees — RuPay cards typically have lower joining and annual fees due to lower processing costs.

- You hold a Jan Dhan, Kisan, or government-scheme linked bank account

Choose Amex if:

- You are a high spender (₹5L+ annually on the card)

- You value lounge access, concierge, and premium lifestyle benefits

- You can handle slightly lower merchant acceptance in tier-2 and tier-3 cities

The smartest users in 2026 hold two cards - typically a RuPay card for domestic UPI-linked spending and a Visa or Mastercard for international and high-value purchases. This setup maximises rewards and reduces decline risk.